BWP TRUST ANNUAL REPORT 2015

45

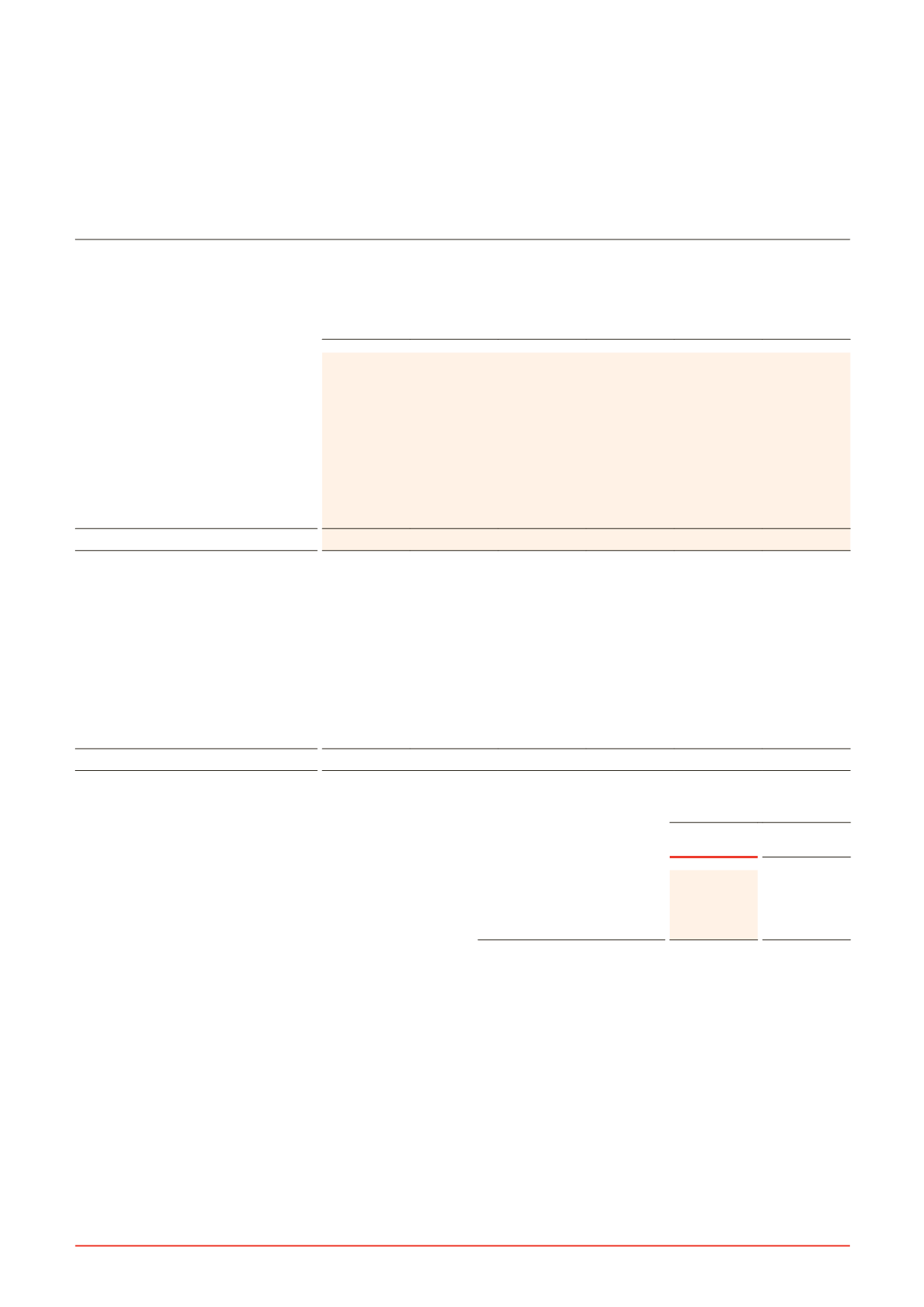

13. FINANCIAL RISK MANAGEMENT (CONTINUED)

Carrying

amount

$000

Contractual

cash flows

$000

1 year

$000

1-2 years

$000

2-5 years

$000

More than

5 years

$000

30 June 2015

Non-derivative financial liabilities

Bank loans - principal

(285,700)

(285,700)

-

-

(193,500)

(92,200)

Bank loans - future interest

-

(42,439)

(9,289)

(9,204)

(23,602)

(344)

Corporate bonds

(199,701)

(236,000)

(9,000)

(9,000)

(218,000)

-

Payables and deferred income

(27,363)

(27,363)

(27,363)

-

-

-

Derivative financial liabilities

Interest rate swaps

(10,943)

(11,400)

(4,295)

(3,520)

(3,389)

(196)

(523,707)

(602,902)

(49,947)

(21,724)

(438,491)

(92,740)

30 June 2014

Non-derivative financial liabilities

Bank loans - principal

(248,938)

(249,200)

-

-

(249,200)

-

Bank loans - future interest

-

(31,919)

(9,998)

(10,484)

(11,437)

Corporate bonds

(199,394)

(245,000)

(9,000)

(9,000)

(227,000)

-

Payables and deferred income

(15,647)

(15,647)

(15,647)

-

-

-

Derivative financial liabilities

Interest rate swaps

(12,047)

(12,621)

(4,406)

(3,924)

(4,122)

(169)

(476,026)

(554,387)

(39,051)

(23,408)

(491,759)

(169)

c) Interest rate risk

Interest rate risk is the risk that the Trust’s finances will be adversely

affected by fluctuations in interest rates. To help reduce this risk in

relation to bank loans, the Trust has employed the use of interest

rate swaps whereby the Trust agrees with various banks to exchange

at specified intervals, the difference between fixed rate and floating

rate interest amounts calculated by reference to an agreed notional

principal amount. Any amounts paid or received relating to interest rate

swaps are recognised as adjustments to interest expense over the life

of each contract swap, thereby effectively fixing the interest rate on the

underlying obligations.

At 30 June 2015 the fixed rates varied from 3.10 per cent to 5.70

per cent (2014: 3.10 per cent to 5.77 per cent) and the floating rates

were at bank bill rates plus a bank margin.

The Trust has a policy of hedging the majority of its borrowings against

interest rate movements to ensure stability of distributions. At 30 June

2015, the Trust’s hedging cover (interest rate swaps and fixed rate

corporate bonds) was 78 per cent of borrowings. This level is currently

above the Board’s preferred 50 per cent to 75 per cent range due to

the corporate bond issuance in late May 2014. Hedging levels are

expected to return within the Board’s preferred range in the coming

years as the Trust continues to grow.

The Trust’s exposure to interest rate risk for classes of financial assets

and financial liabilities is set out as follows:

Carrying amount

June 2015

$000

June 2014

$000

Variable rate instruments

Cash and short-term deposits

32,445

12,045

Bank debt facilities

(285,700)

(248,938)

The Trust’s sensitivity to interest rate movements

Fair value sensitivity analysis for fixed rate instruments

The Trust does not account for any fixed-rate financial assets or

financial liabilities at fair value through the profit or loss, and the Trust

does not designate any interest rate swaps as hedging instruments

under a fair value hedging model. Therefore, a change in interest rates

at the reporting date would not affect profit or loss.

Cash flow sensitivity analysis for variable rate instruments

The analysis on the following page considers the impact on equity and

net profit or loss due to a reasonably possible increase or decrease in

interest rates. This analysis assumes that all other variables remain

constant. The analysis is performed on the same basis for 2014.