BWP TRUST ANNUAL REPORT 2015

7

PROFIT

Profit as disclosed in the Trust’s financial statements includes

unrealised gains or losses in the fair value of investment properties

as a result of the revaluation of the entire property portfolio every

six months (see revaluations section in Our property portfolio).

The unrealised revaluation gains or losses are recognised as

undistributed income as part of unitholders’ equity in the financial

statements and do not affect the profit available for distribution to

unitholders each period.

For the year ended 30 June 2015, net profit was $210.1 million,

including $108.5 million in gains in the fair value of investment

properties. This compares with $149.1 million last year, including

gains of $57.1 million in the fair value of investment properties.

Distributable profit for the year (excluding revaluation gains or

losses) was $101.6 million, compared to $92.8 million (including

$0.8 million partial distribution of capital profits) for the year ended

30 June 2014.

FINANCIAL POSITION

As at 30 June 2015, the Trust’s total assets were $2,018.0 million

(2014: $1,837.4 million) with unitholders’ equity of $1,441.8

million and total liabilities of $576.2 million. Investment properties

and assets held for sale made up the majority of total assets,

comprising $1,981.3 million (2014: $1,819.0 million). Details of

investment properties are contained in the Our property portfolio

section at pages 12 to 17.

The underlying net tangible asset backing of the Trust’s units

(“NTAâ€) as at 30 June 2015 was $2.24 per unit, an increase of

2.8 per cent from $2.18 per unit as at 31 December 2014 and 8.2

per cent from $2.07 per unit as at 30 June 2014. The increase in

NTA over the 12 months to 30 June 2015 was due to the increase

in net assets through property revaluations.

DISTRIBUTION TO UNITHOLDERS

The Trust pays out 100 per cent of distributable profit each

period, in accordance with the requirements of the Trust’s

constitution. A final distribution of 8.17 cents per ordinary unit

has been declared and will be made on 27 August 2015 to

unitholders on the Trust’s register at 5.00 pm (AEST) on 30 June

2015. The final distribution takes the total distribution for the

year to 15.84 cents per unit (2014: 14.71 cents per unit). The tax

advantaged component of the distribution is 18.27 per cent, lower

than in previous years due to the property divestments, and

taxable capital gains resulting from them.

Units allocated under the Trust’s Distribution Reinvestment Plan

(“DRPâ€) in respect of the final distribution will be allocated at

$3.2561 per unit, representing the average of the daily volume

weighted average price of the Trust’s units for the 20 trading days

from and including 6 July 2015 to 31 July 2015, with no discount

applied. Units to be allocated under the DRP were acquired on

market and will be transferred to participants on 27 August 2015.

CAPITAL MANAGEMENT

The Trust is committed to maintaining a strong investment

grade rating (currently A-/Stable/- Standard & Poor’s) through

appropriate capital and balance sheet management.

DEBT FUNDING

During the year, the Trust repriced and extended all of its bi-lateral

banking facilities.

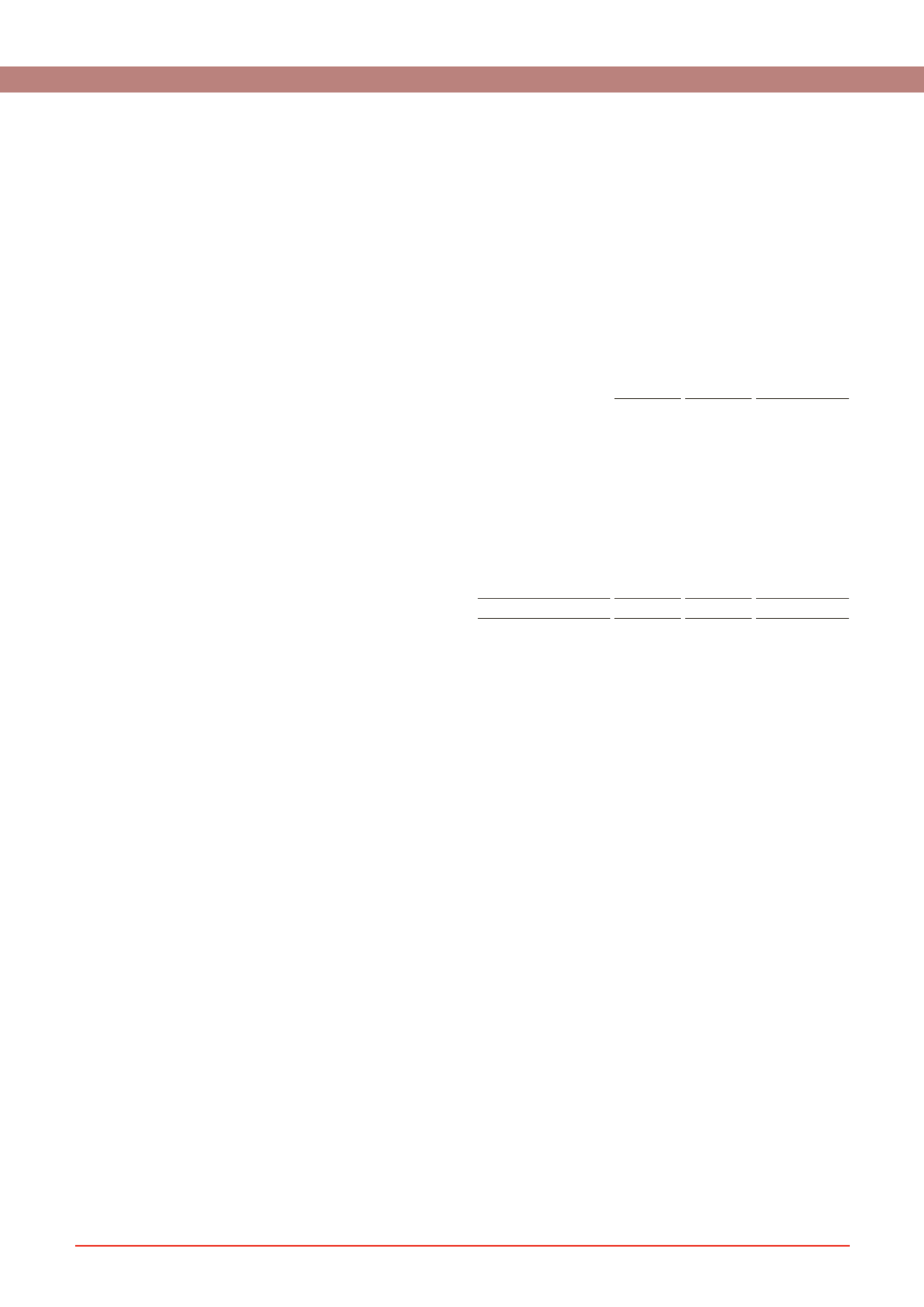

The Trust’s debt facilities as at 30 June 2015 are summarised below.

Limit

$m

Amount

drawn

1

$m

Expiry

date

Bank debt facilities

Australia and New

Zealand Banking Group

Limited

110.0

94.3

1 July 2018

Commonwealth Bank

of Australia

110.0

92.2 31 July 2020

Westpac Banking

Corporation

135.0

99.2 30 April 2020

Corporate bonds

Fixed term five-year

corporate bond

200.0

200.0 27 May 2019

Total

555.0

485.7

1

Amount drawn includes prepaid interest and borrowing costs of $0.3 million

as at 30 June 2015 on debt facilities

As at 30 June 2015, the weighted average duration of the Trust’s

debt facilities was 4.2 years to expiry (2014: 3.7 years) and

average utilisation of debt facilities (average borrowings/average

facility limits) for the year was 80.4 per cent (2014: 74.2 per cent).

In respect of the Trusts’ bank debt facilities, whilst these have fixed

maturity dates, the terms of these facilities allow for the maturity

period to be extended by a further year each year subject to the

amended terms and conditions being accepted by both parties.

DISTRIBUTION REINVESTMENT PLAN

The DRP was in place for both the interim distribution and

final distribution for the year ended 30 June 2015. The Trust

has continued to maintain an active DRP as a component of

longer-term capital management and to allow unitholders

flexibility in receiving their distribution entitlements. The DRP

provides a measured and efficient means of accessing additional

equity capital from existing eligible unitholders.

INTEREST RATE MANAGEMENT

The Trust takes out interest rate swaps and fixed rate corporate

bonds (hedging) to create certainty of the interest costs of the

majority of borrowings over the medium to long-term. As at 30 June

2015, the Trust’s interest rate hedging cover was 78.2 per cent of

borrowings (outside the Board preferred range of 50 to 75 per cent),

with $180.0 million of interest rate swaps and the $200.0 million

fixed rate corporate bond, against interest bearing debt of $485.7

million. The weighted average term to maturity of hedging was 3.17

years, including delayed start swaps.